see

Home

see

Home

- see

News

- see

Geothermal Energy Sector Is Set For Growth Due To Positive Market Drivers And The Backing Of Oil

see

News

Thought Leadership Piece for Petroleum Economist Outlook 2024

Geothermal Energy Sector is set for Growth due to positive Market Drivers and the backing of Oil and Gas Suppliers.

Introduction

Geothermal energy is experiencing a renewed resurgence of interest and investment as governments at a national and local level work to decarbonise their energy mix away from an over reliance on hydrocarbons. The geothermal industry last saw significant investment following the oil supply shocks of the 1970’s but has until now largely remained confined to regions with particularly high geothermal gradients, marked by high volcanic activity such as countries around the Pacific.

With the energy transition a key focus for policymakers geothermal has returned as an attractive clean and renewable energy source. A key advantage of geothermal over other renewable solutions lies in its reliability, as it can produce a constant supply of energy 24/7, in contrast to the intermittent nature of wind and solar. The capability to provide a reliable baseload of power and heat supply ensures geothermal will be a critical element of future energy systems.

For power generation, as well as increased drilling in conventional hydrothermal reservoirs there is an active program of exploratory drilling to access so called enhanced geothermal systems (EGS) through deep drilling with hydraulic fracturing to enhance the resource potential. This has the potential to open up new regions to geothermal. Geothermal can also be an attractive energy source for domestic and industrial heating, which represents a significant source of hard to abate Co2 emissions (in the UK heating accounts for about 37% of total UK carbon emissions (CCC 2022)).

Key Growth Drivers

The recent energy crisis has brought energy security and energy affordability into sharp focus for governments and consumers across the world. Government incentives have played a pivotal role in fast tracking the move to clean energy production. In the USA the Inflation Reduction Act (IRA), in addition to curbing inflation has provided significant stimulus through tax credits to promote investment in clean energy. In turn, the EU has outlined its Green Deal Industrial Plan which similarly aims to incentivise the adoption of clean energy. As the energy transition has gathered pace there has been a notable trend of oil and gas suppliers looking to reposition themselves and diversify toward supporting more sustainable energy sources. In geothermal they have seen an opportunity to leverage their experience and skills in terms of sub-surface formation evaluation, drilling, and more efficient use of the technology necessary for cost effective injection and production of fluids to surface.

Even before the IRA, the USA was the global leader in geothermal energy, with California and Nevada, both endowed with high geothermal gradients, producing around 6% and 10% respectively of their electricity from geothermal. Other global ‘hotspots’ are to be foundin Iceland, Kenya, Turkey and some APAC countries including Philippines, Indonesia and New Zealand.These countries are ideally located close to geological zones of relatively shallow high heat flow.In Europe development of geothermal district heating networks is making great strides, most notably in countries such as Denmark, the Netherlands, France and Germany. Development of exciting next generation geothermal extraction technologies strives to attain the possibility of geothermal everywhere.

Supported by Leaders in the Oil & Gas Industry

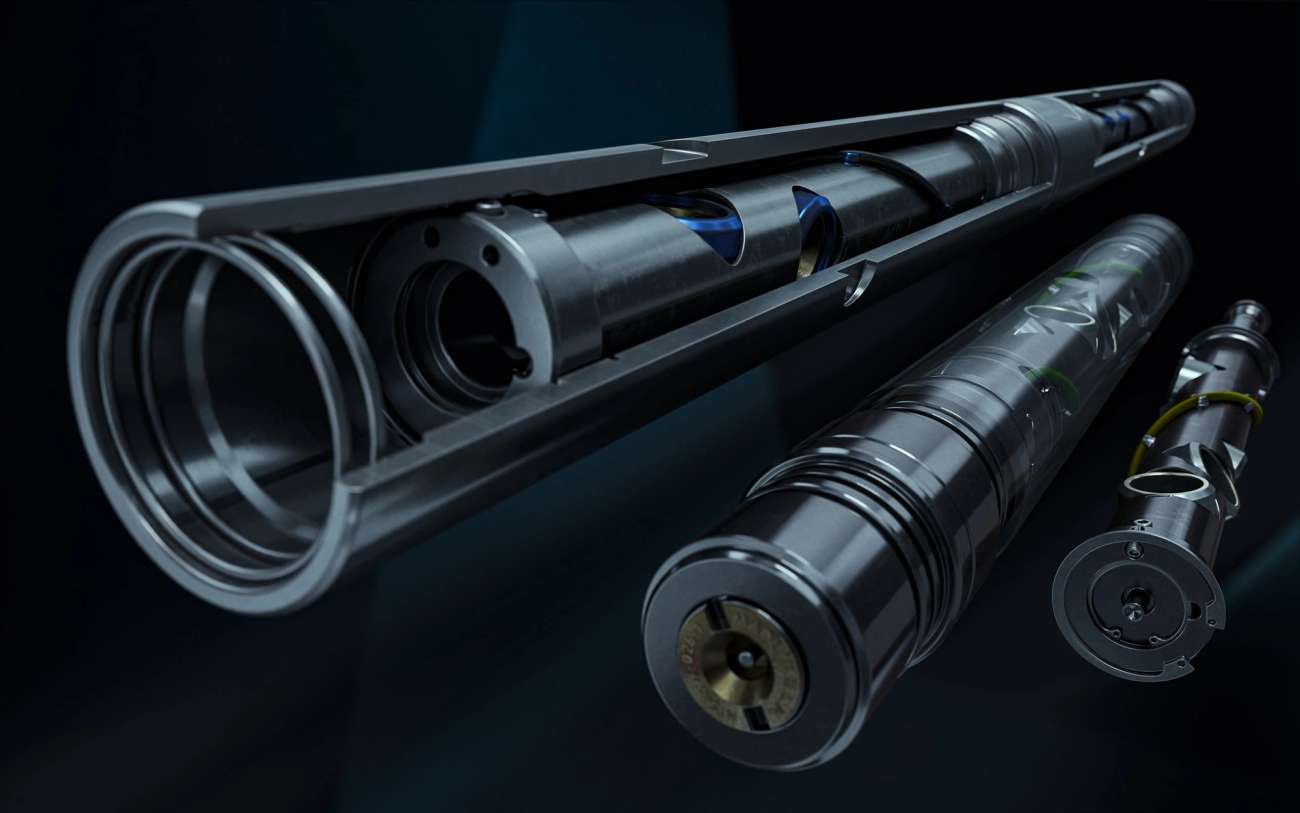

Hunting plc (Hunting), a global leader in the provision of services to the energy sector, with an established history supplying Oil Country Tubular Goods (OCTG), downhole perforating systems and other specialist equipment to the oil and gas industry forecasts significant growth in geothermal activity. In fact, Hunting has been supporting geothermal projects for decades, but they have now observed a significant uptick in business activity across the key geothermal market areas in the US, APAC region and Europe. The endorsement of major oil and gas operators, such as in the case of Eavor, backed by the likes of bp and OMV, Fervo Energy’s collaboration with Devon Energy and Chevron’s JV with Baseload Capital, signifies a step-change in the capabilities and ambitions to make geothermal a bigger part of the energy mix.

Ambitious Targets will Drive Investment and Growth

This year in California, the California Public Utilities Commission (CPUC) approved an ambitious plan that aims to add 2GW of geothermal power plants representing over double the States’ current geothermal power production of c.a. 1900MW. Ambitious targets set in California and other regions have bolstered investor confidence in the geothermal energy sector. This growing confidence has inspired companies like Eavor and Fervo Energy to push the boundaries of traditional geothermal drilling techniques in pursuit of Advanced Geothermal Systems (AGS) and EGS respectively.In their endeavours, they draw upon techniques and technology derived from the oil and gas industry to achieve their goals.

Temperatures downhole in some of the hottest geothermal wells can reach over 620° F, with fluids often being highly corrosive under these superheated steam conditions. This environment requires exotic corrosion resistant materials that can withstand these extremely challenging conditions. Providing a safe and reliable well infrastructure for production of superheated steam up to surface power plants and reinjection of cooler fluid back down to superhot rock formations, thus resuming the cycle.

Leveraging Oil & Gas HPHT and Advanced Well Construction Experience

Hunting is leveraging its significant experience in OCTG and metal to metal sealing premium connections that maintain well integrity and extend the lifespan of these wells, alongside the use of advanced materials with its experience in subsea technology and precision manufacturing of critical components used in aerospace and space industries. The oil and gas industry has overcome numerous technical challenges to reach deeper and deeper depths to produce high press high temperature (HPHT) hydrocarbons and has pioneered critical directional drilling and completion technologies. These advancements in HPHT and Unconventional Oil and Gas technologies can now help drive geothermal to the next level, increasing the geothermal potential that can be harnessed.

Significant Growth Potential

The geothermal sector is primed for growth, with strong market drivers supporting its development as a key component of strategies to achieve Net Zero targets. Increased investment and leveraging of the oil and gas industry’s experience and technology means new techniques can propagate into areas where previously geothermal was deemed unworkable. This opens up the opportunity to develop a reliable clean energy source and help to reduce carbon emissions from hard to abate energy sectors.

Credit - This article first appeared in PE Outlook 2024 (available here)